Increase Your Returns Without Changing your Gross Income or Expenses.

There are three truths in Real Estate Investing:

1) There are tax advantages that no other form of investments offer

2) Use leverage to increase returns

3) You originally bought the real estate as an investment, as such, you should treat it as such and analyze, at least on a bi-annual basis, whether there are better investments you should invest in.

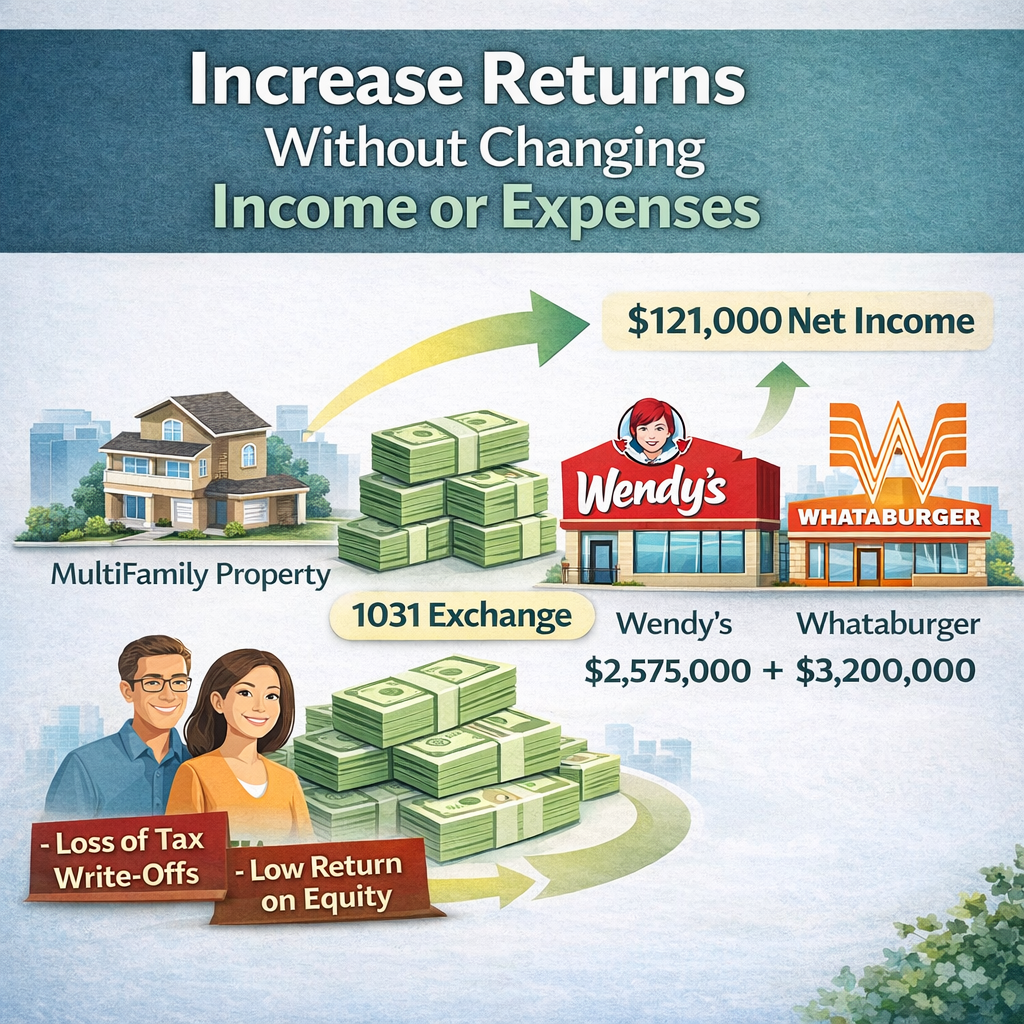

Meet Mr. and Mrs. Sanchez. When I first met them, they had a multi-family property that they had owned for over 25 years. They thought their investment was doing well. They had paid $250,000 for it, had paid off the original loan, and it was now generating $120,000 in net income (pre-tax), a 48% annual return on their original investment. Sounds good right? It does until you factor in the appreciation and the true value of the property. When we looked at that, we realized that the property was worth about $3,200,000, showing a true annual cash on equity return of only 3.75%. They had gained almost $3,000,000 in equity, equity that wasn’t working for them.

Additionally, by paying off the loan, they didn’t have any interest to write off, and they had in fact fully depreciated the property.

We discussed different investment strategies with their C.P.A. and came to the conclusion that their investment would be better off if they sold it, and repositioned into one or two other assets. They decided to move forward and put their property on the market. We eventually sold it for $3,250,000, after costs of sale, they were left with just over $3,000,000 in cash. The proceeds from the sale was placed with an accommodator for a tax deferred 1031 exchange. Now the search was on.

We actually located two Single Tenant Net Lease (“STNL”) properties for them. One was a Corporate Wendy’s in Tennessee, and the other a What-A-Burger in Texas. Both in well located, in-fill areas. Both with long-term NNN leases. We were able to acquire the Wendy’s at $2,575,000 at a 5.2% CAP Rate and the What-A-Burger at $3,200,000, at a 5.0% Cap Rate, both corporate guaranteed. Net Operating income before debt service was $295,187. But wait, how much did the debt cost them?

The Sanchez’s were concerned about risk, so we went in with very low leverage, just at 50%. With the current rates at the time, they were able to secure a 10 year fixed rate, with monthly payments about $15,300, or $183,600 annually. Your probably saying, wait, how does that math add up? If they were getting $295,187 in Net Operating Income, after subtracting the annual mortgage payment, that only left them with $111,587, which is less than the $120,000 they were making. Well that’s where the power of leverage, as well as depreciation come in.

Their original investment brought in $120,000 in net income a year, with no write offs. With their other income this actually pushed them into a higher tax bracket (24% Federal, and 9.3% State, for a total tax bracket of 33.3%). This left them with actual cash in pocket of about $80,000.

Now, with the new investment, they had net income of $111,587. They were able to increase their basis by about $2,000,000, giving them a $51,282 write off. Due to the write offs, they were actually in a slightly lower tax bracket overall (22% Federal, but still 9.3% for State) leaving them with about $76,000 in cash in pocket (plus any additional from the tax savings on their other income).

In addition, part of the loan payment went to pay off the loan, this is what is known as Gain On Equity. This amount averaged about $45,000 year over the 10 year period. So, not only did they pay less tax they also received a benefit of the gain-on-equity, bringing their total return to over $121,000 (after taxes), an increase of about 50% from their other investment. They also had the additional benefit of leveraged appreciation with the new investment. All in all a win-win proposition.

If you take anything away from this white paper I’d like it to be this: whether you’re investing in stocks, real estate, or anything else for that matter, you should always evaluate how your investment is doing, taking into consideration everything that may impact your return, and if there is a better option for that investment, then way the risk, and make an informed decision on moving forward. If you’re looking to reinvest, or just want to know how your real estate investment is looking compared to other options, please do not hesitate to reach out to me at gpino@cbicommercial.com